One of my readers, OregonSun sent me an email about a recent loan asking, “We have a loan that is on simple interest. Even though we are making double the payments, the balance (interest we are paying) doesn't seem to be reducing the way I thought it would. Am I doing something wrong?”

I asked for a few more details, and said I would take a look.

OregonSun says she is her most recent payment was $90.20 and the interest was $31.24.

One of my favorite spreadsheets from Vertex42 is the Loan Amortization Calculator, available free for personal use.

I put the amounts into the spreadsheet to get a look at the schedule.

Since OregonSun said the payment was $90.20 and this Amortization Calculator says it should be $89.77, I would suspect some type of additional fees.

Next, take a look at “Total Payments” amount – this includes the interest that will be paid over the life of the loan. $5386.33. The interest will be $1036.33. The loan is for five years, so the number of loan payments is 60.

OregonSun says they have are paying $100 twice a month. The Loan Amortization Calculator only allows us to put in a total extra amount paid per month so I have entered one payment plus $200 and let's see what it looks like now.

Now we can see that by making an extra payment of $200 in addition to the regular monthly payment, the payments left have been reduced by 3. Instead of seeing 59 payments (one payment has been made, there were 60 total to begin with), there are only 57 left.

The interest left to be paid over the life of the loan – if OregonSun never made another extra payment, has dropped to $932.06 from $1036.33 (a savings in interest of $104.26).

Instead of the total cost of the unit being $5386.33 (including interest), it has dropped to $5282.06.

Now let's see how it looks when they make that $200 extra payment for February:

This is the second month, if no extra payments had been made, two payments would have been made, leaving 58 payments. But now we see there are only 54 payments left.

The interest left to be paid over the life of the loan – if OregonSun never made another extra payment, has dropped to $837.08 from $1036.33 (a savings in interest of $199.24).

Instead of the total cost of the unit being $5386.33 (including interest), it has dropped to $5187.08.

Now let's see how it looks when they make that $200 extra payment for March:

This is the second month, if no extra payments had been made, three payments would have been made, leaving 57 payments. But now we see there are only 51 payments left.

The interest left to be paid over the life of the loan – if OregonSun never made another extra payment, has dropped to $751.07 from $1036.33 (a savings in interest of $285.25).

Instead of the total cost of the unit being $5386.33 (including interest), it has dropped to $5101.07.

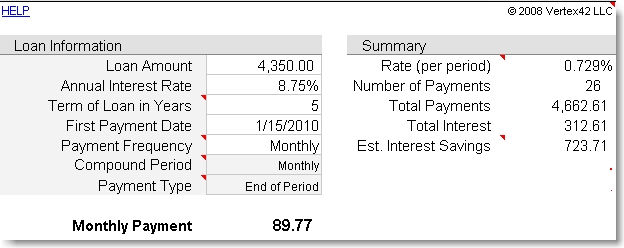

Now let's jump ahead and see how it looks after they have made 12 extra payments of $200/month.

{kind=link}

This is the twelfth month, if no extra payments had been made, twelve payments would have been made, leaving 48 payments. But now we see there are only 26 payments left.

The interest left to be paid over the life of the loan – if OregonSun never made another extra payment, has dropped to $312.61 from $1036.33 (a savings in interest of $723.71).

Instead of the total cost of the unit being $5386.33 (including interest), it has dropped to $4662.61.

Now let's jump ahead and see how it looks after they have made 12 more extra payments of $200/month.

Guess what? If they continue to pay $200 a month, they would be done long before 12 months! It would take only four more weeks to pay off that loan – and the last extra payment would only be $187.52.

Here is a shot including the bottom part of the calculator – which is where you get to see more of the fun details:

Now OregonSun's original question was why the interest didn't seem to be dropping as fast as she thought it would. The interest doesn't drop so fast in the beginning because the principal is higher. But if you make additional (large) payments over time, it will eventually drop in the monthly payment. You will see that over time the amount of interest you were expecting to pay initially will be significantly lower.

In OregonSun's case, as long as she keeps up with those extra payments at $200 a month, she will save $762.48 in interest.

And the loan will be gone in 16 months, instead of 60 months!

If you don't have Microsoft Excel, head on over to OpenOffice and download their free Office suite, which includes their version of Excel, called Calc. Vertex42 usually states whether the spreadsheet is known to work in OpenOffice, and does not indicate on this calculator. However, I opened it in Calc and it seemed to work just fine.

I hope this helps, OregonSun.

Yours Truly,

You are the spreadsheet queen!

[Reply]

Mrs. Accountability Reply:

March 6th, 2010 at 8:20 pm

Wow, Mr. Credit Card… no wait, I’m not the one that made that spreadsheet. I just know how to put numbers into it. I do know a fair amount about Excel though and do like working with the program.

[Reply]

This may sound stupid but did they specify to have the double payment applied towards the principal? Many times, if you make an extra payment without any other information, the amount is simply applied towards the next payment due. I don’t know. This may be a question to ask the person.

[Reply]

Mrs. Accountability Reply:

March 6th, 2010 at 8:24 pm

Dirac: I am not sure – hopefully OregonSun will respond and let us know.

[Reply]

One thing popped out at me when reading this. She isn’t making double payments. She is making 2 payments a month correct? Is the company putting all of the second payment to principal reducting or just assuming she is paying a monthly payment, therefore applying the second $100 payment to interest and principal like a regular monthly payment. Something to look into. It might be better to make 1 payment of $200 a month rather than 2 separate payments.

[Reply]

Mrs. Accountability Reply:

March 6th, 2010 at 8:26 pm

Jennifer, these are all good questions for OregonSun to think about and look into. Thanks for the suggestions!

[Reply]